Pionex Card pays 1% cashback in USDT on every eligible purchase with no monthly cap. Here is what that actually means in real money, across different spending amounts, combined with the 5% APR on your card balance.

Cashback on crypto cards is usually either too complicated or too good to be true. The 8% rates require staking thousands of dollars in a token you do not want. The simple flat rates are capped at $25 a month. The “unlimited” programmes turn out to have exclusion lists three pages long.

Pionex Card’s cashback is 1%, uncapped, in real USDT. No staking. No tier. No token. No expiry. The question is whether 1% is actually meaningful, or whether it is a marketing number that sounds good but adds up to almost nothing.

The answer depends on how much you spend and how much you keep in the card account. This article does the maths honestly across several spending profiles, combines the cashback with the 5% APR on card balances, and explains exactly what you lose or gain compared to spending with no rewards at all.

For the full fee schedule and card overview, read the main review: Pionex Card: The Crypto Card That Actually Pays You Back.

Contents

- 1 How the Cashback Actually Works

- 2 The Annual Maths: Four Spending Profiles

- 3 The FX Fee Offset: Why It Matters More Than It Looks

- 4 The 5% APR: The Feature Most Users Underestimate

- 5 What Partially Reduces the Cashback Value

- 6 Is 1% Cashback Competitive?

- 7 Cashback + APR Combined: The Full Return Picture

- 8 Practical Example: A Malaysia-Based User

- 9 Frequently Asked Questions

- 10 The Honest Answer

How the Cashback Actually Works

Every eligible purchase earns 1% back in USDT, credited directly to your card account. Not points toward a future redemption. Not a percentage off next month’s bill. Real USDT, sitting in your account after each transaction.

A few things worth knowing from the official programme terms:

What earns cashback: Most eligible purchases at Visa-accepting merchants, both online and in-store through linked wallets.

What does not earn cashback: ATM withdrawals. A small number of specific merchants including eToro, TikTok, and Wise. Check the Cashback Programme Guidelines in the Pionex app for the current exclusion list.

Refund handling: If you return a full purchase, the cashback on that transaction is reclaimed. If you return part of a purchase, the cashback is clawed back proportionally. For a partial refund, the formula is: cashback reclaimed = original cashback × (refund amount / original transaction amount).

The FX offset: On non-USD purchases using the Visa card, a 1% foreign exchange fee applies. The 1% cashback offsets this exactly on eligible transactions. The net result on international spending is zero FX cost. This is not a coincidence. It is the design.

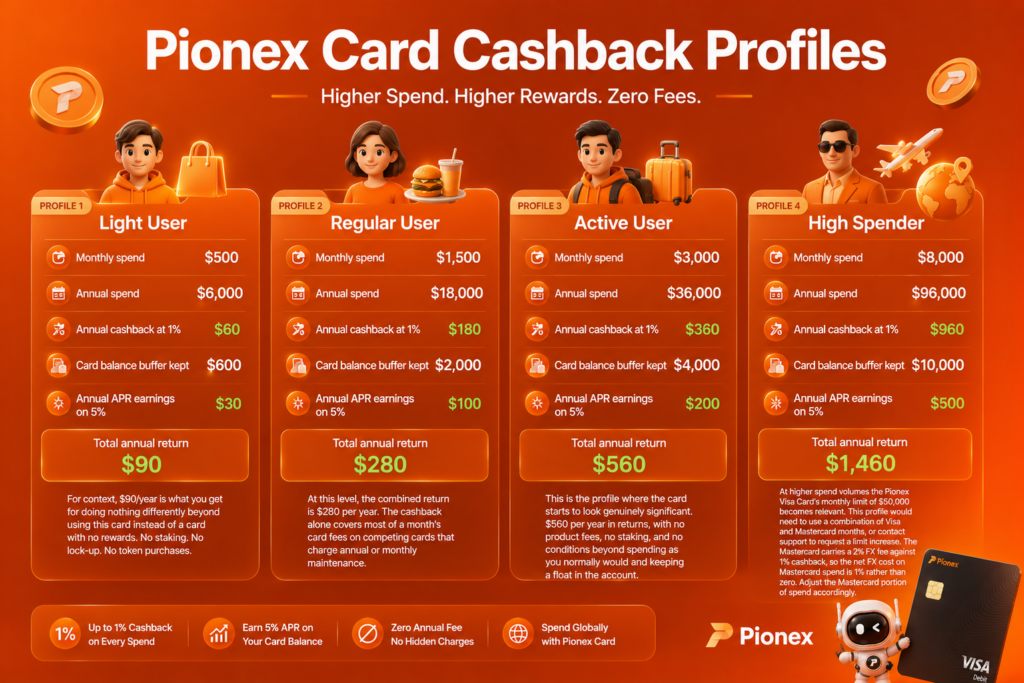

The Annual Maths: Four Spending Profiles

All figures below use the official Pionex Card fee schedule. Cashback is calculated at 1% on the transaction amount after the 1% FX fee. For simplicity, these examples assume all purchases are eligible for cashback.

Profile 1: Light User — $500/month in spending

Monthly spend: $500

Annual spend: $6,000

Annual cashback at 1%: $60

Card balance buffer kept: $600 (roughly one month of spend)

Annual APR earnings on $600 at 5%: $30

Total annual return: $90

For context, $90/year is what you get for doing nothing differently beyond using this card instead of a card with no rewards. No staking. No lock-up. No token purchases.

Profile 2: Regular User — $1,500/month in spending

Monthly spend: $1,500

Annual spend: $18,000

Annual cashback at 1%: $180

Card balance buffer kept: $2,000

Annual APR earnings on $2,000 at 5%: $100

Total annual return: $280

At this level, the combined return is $280 per year. The cashback alone covers most of a month’s card fees on competing cards that charge annual or monthly maintenance.

Profile 3: Active User — $3,000/month in spending

Monthly spend: $3,000

Annual spend: $36,000

Annual cashback at 1%: $360

Card balance buffer kept: $4,000

Annual APR earnings on $4,000 at 5%: $200

Total annual return: $560

This is the profile where the card starts to look genuinely significant. $560 per year in returns, with no product fees, no staking, and no conditions beyond spending as you normally would and keeping a float in the account.

Profile 4: High Spender — $8,000/month in spending

Monthly spend: $8,000

Annual spend: $96,000

Annual cashback at 1%: $960

Card balance buffer kept: $10,000

Annual APR earnings on $10,000 at 5%: $500

Total annual return: $1,460

At higher spend volumes the Pionex Visa Card’s monthly limit of $50,000 becomes relevant. This profile would need to use a combination of Visa and Mastercard months, or contact support to request a limit increase. The Mastercard carries a 2% FX fee against 1% cashback, so the net FX cost on Mastercard spend is 1% rather than zero. Adjust the Mastercard portion of spend accordingly.

The FX Fee Offset: Why It Matters More Than It Looks

Most people focus on cashback as a bonus. The more important function for international users is what the cashback does to the FX fee.

Every non-USD purchase on the Pionex Visa Card carries a 1% foreign exchange fee. Without cashback, that fee is a straight cost. A user spending $2,000/month internationally pays $240/year in FX fees, full stop.

The 1% cashback offsets that 1% FX fee exactly on eligible purchases. The net FX cost drops to zero.

Compare this to what you pay with alternatives:

| Card | FX Fee | Cashback | Net Annual Cost on $24,000/year international spend |

| Pionex Visa | 1% | 1% | $0 |

| RedotPay | 2.2% | None | $528 |

| Standard bank debit card | 1.5–3.5% | None | $360–$840 |

| Typical travel credit card | 0% | Varies | $0 (but annual fee often $95–$550) |

For a user spending $2,000/month internationally with no crypto card at all, moving to Pionex Card saves between $360 and $840 per year just on FX fees, before counting any cashback return.

The 5% APR: The Feature Most Users Underestimate

The cashback is easy to understand. The APR is the part people tend to overlook.

Whatever USDT is sitting in your Pionex Card account earns 5% annually. It accrues continuously. There is no lock-up, no minimum balance beyond the 100 USDT needed to apply, and no requirement to keep the funds sitting idle. You can transfer in and out as needed.

From the official fee schedule, this is described as interest on the card account balance with no restriction on withdrawal timing. The rate is subject to change, so check the current figure in the app.

What this means practically: the card account is not just a spending wallet. Any float you maintain there is earning while it waits to be spent. This is distinct from keeping funds in your main Pionex trading account, where they may be deployed in bots or earn products but are not as liquid for card spending.

A $3,000 buffer earns $150/year at 5% APR. A $5,000 buffer earns $250/year. Combined with cashback on spending, the total return for a user maintaining a reasonable float starts to look meaningful.

What Partially Reduces the Cashback Value

It is worth being clear about the situations where the cashback does not fully play out.

Refunds: Full refunds reclaim the entire cashback. If you buy and return a lot, the effective cashback rate drops. For regular purchases you keep, this is not a factor.

Small transaction fees: Purchases of 1 USD or less are subject to a small transaction fee structure. The first one per person per month is free. After that, 0.2 USDT per transaction. If you make a lot of sub-dollar purchases, the 0.2 USDT fee can exceed the cashback earned on that transaction. For most spending patterns, this is a minor edge case.

Mastercard vs Visa: If you use the Mastercard variant, the FX fee is 2% against 1% cashback, leaving a net 1% FX cost on non-USD purchases. For heavy international spenders, the Visa card is the better option specifically because the cashback and FX fee cancel out completely.

Excluded merchants: eToro, TikTok, and Wise are confirmed excluded from cashback. The full list is in the app. Check it if those platforms are significant in your spending.

Is 1% Cashback Competitive?

Compared to other crypto cards targeting the same tier of user:

RedotPay: No cashback at all on standard cards. Pionex wins outright.

Bybit Card: Headlines at 10% but caps at $10 per month for standard accounts. That is 0.5% on $2,000 of monthly spend. Pionex’s uncapped 1% beats this for anyone spending more than $1,000/month.

KAST Card: Seasonal cashback rates that change quarterly. Season 5 offered 6% in MOVE tokens. The conversion from MOVE tokens to spendable value adds steps and uncertainty. Pionex pays directly in USDT with no conversion required.

Traditional bank cards: Most flat-rate cashback cards pay 1 to 2% in the markets where Pionex Card operates (Malaysia, Singapore, Germany, etc.). Pionex at 1% is in range with no annual fee to offset, which changes the net comparison significantly. A bank card paying 1.5% but charging $95/year in annual fees needs $6,333 in annual spend to break even on the fee before any reward has real value.

Cashback + APR Combined: The Full Return Picture

Most cashback comparisons look at spend rewards in isolation. The Pionex Card case is better made by combining both return streams.

| Monthly Spend | Annual Cashback | Buffer Kept | Annual APR (5%) | Total Annual Return |

| $500 | $60 | $600 | $30 | $90 |

| $1,000 | $120 | $1,200 | $60 | $180 |

| $1,500 | $180 | $2,000 | $100 | $280 |

| $2,500 | $300 | $3,000 | $150 | $450 |

| $3,000 | $360 | $4,000 | $200 | $560 |

| $5,000 | $600 | $6,000 | $300 | $900 |

These numbers assume no annual fee because there is none, no issuance fee because there is none, and no staking requirement because there is none.

The buffer figures above are conservative estimates. If you keep a larger float, the APR return scales with it independently of spending.

Practical Example: A Malaysia-Based User

Malaysia is one of the top countries by Pionex Card AI search traffic. Here is what the card looks like for a typical use case there.

A user in Kuala Lumpur spends roughly 2,000 MYR per month on everyday purchases including groceries, online shopping, subscriptions, and dining. At current exchange rates (approximately 4.4 MYR per USD), that is around $455 USD monthly.

- Annual spend in USD equivalent: ~$5,460

- Annual cashback at 1%: ~$54.60 in USDT

- Card buffer maintained: $600 (about 2,640 MYR)

- Annual APR on buffer at 5%: $30

- Total annual return: ~$84.60

Every transaction at a non-MYR merchant or USD-priced platform (common for SaaS, streaming, online shopping) earns cashback with the FX fee offsetting exactly. Transactions in MYR at local merchants are subject to the 1% FX fee, offset by 1% cashback.

Net result: a Malaysian user keeping a reasonable buffer earns approximately $85/year from a card with no annual fee and no staking requirement.

Frequently Asked Questions

How is the 1% cashback calculated?

Cashback is calculated as 1% of the transaction amount in USDT. If you spend 50 MYR, the equivalent USDT amount at the Visa exchange rate is calculated, and 1% of that figure is credited to your card account.

When is the cashback credited?

Cashback is credited to your card account after the transaction is confirmed. It does not appear as a pending amount during pre-authorisation holds.

Is the cashback credited in USDT or another currency?

USDT only. It goes directly into your Pionex Card account balance.

Does the cashback expire?

No. Once credited to your card account, it stays there. There is no expiry on USDT in your account.

Can I withdraw the cashback?

The USDT in your card account can be transferred back to your main Pionex account and then withdrawn through the standard process.

What happens to cashback if I refund a purchase?

Full refund: the entire cashback for that transaction is reclaimed. Partial refund: cashback is reclaimed proportionally based on the refunded amount as a percentage of the original transaction.

Does the 5% APR apply to the cashback USDT in my account?

Yes. Any USDT in your card account earns 5% APR, including cashback that has been credited there.

The Honest Answer

Is 1% cashback worth it on the Pionex Card? Yes, specifically because it does two things at once.

For international spenders, the 1% offsets the 1% FX fee entirely. You are not earning a bonus on top of your costs. You are eliminating a cost that would otherwise exist. That is a different kind of value.

For the cashback itself, 1% uncapped in real USDT is competitive for the crypto card market at this tier. It is not the headline number of some competitor programmes, but those programmes either require staking, cap the monthly return low, or pay in tokens you then have to convert. Pionex pays in USDT, no conditions.

The 5% APR on your card balance is the feature that makes the full picture compelling. Combined with cashback, the total annual return for a user spending $1,500/month and keeping a $2,000 buffer is around $280 per year, from a product with no annual fee and no staking requirement.

Whether that justifies moving spending to this card depends on what you are using now. If you are using a bank card with 0% cashback and 2% FX fees, the switch is straightforward. If you are using a premium travel card with 0% FX and 3% rewards but paying $400/year in annual fees, the maths is closer.

For Pionex users already holding USDT, the question is almost rhetorical. The card is free. The cashback is real. The APR runs on whatever float you keep. There is no obvious reason not to use it.

Need setup help? Visit the Pionex Card Support Centre. For country availability, see Where Does Pionex Card Work.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cashback rates, APR, fees, and programme terms may change. Always verify current terms in the Pionex app before making decisions. All calculations are illustrative estimates based on the official Pionex Card fee schedule as of June 2026.